Adhering to the standards and best practices of certifying agencies appointed by the USDA is only one small piece of the complex organic grain production puzzle. In fact, even after successfully implementing organic farming standards, marketing organic grains comes with significant disadvantages compared to conventional grain marketing. The payoff, however, is the possibility of greater farm income—organic grains trade at a premium over their conventional counterparts. And for some conventional growers, this premium is motivation enough to consider the arduous transition to organic farming.

There are three primary disadvantages organic grain farmers face that those who market conventional grains don’t. These challenges may deter some conventional farmers from transitioning to organic production. We’ll briefly outline these disadvantages, and offer some potential work-arounds, too.

#1: Physical Infrastructure Constraints

Most conventional growers have access to multiple local grain elevators and storage options. And with plenty of infrastructure available, it’s easier for them to take advantage of marketing opportunities and leverage competition to find the best price for their grain. Conversely, the organic side of the market has few, sparsely located, elevators and storage options, which leaves many organic growers captive to the requirements and prices of whichever buyer happens to be nearby.

The lack of infrastructure also leads to increased shipping costs for organic farmers due to the lack of nearby handlers. Many organic growers must ship their grain upwards of a hundred miles to the nearest certified organic handling facility, whereas conventional farmers often have several options “just down the road.” For organic producers who can afford to do so, building on-farm storage or handling capacity is an important step towards adding flexibility to their marketing decisions. However, long term, the industry will require more investment in grain transportation and handling infrastructure.

#2 Profit Losses During Transitional Period

The three-year period wherein growers are required to farm organically, despite being unable to capture organic price premiums, creates a significant barrier to transitioning to organic farming. The increased costs associated with organic farming (while not being able to recoup them with higher premiums) almost guarantees growers three years in a row of financial losses. For some growers, this is an untenable option. But some end users, such as Chipotle and General Mills, are paying a premium for transitional ingredients in an attempt to 1) incentivize farmers to transition, and 2) lock down future, long-term organic grain supplies. Broad consumer education about organic farming, the transition process, and transitional ingredients has also been a critical component of such programs. These efforts represent a step in the right direction.

For established transitioning growers, it’s important to initiate planting schedules to best position harvest, if possible, immediately after the organic certification date. Even if a crop was planted while in transition, it will be deemed organic if harvested after the certification date. Transitioning growers may also seek financial or technical assistance from programs such as the USDA’s EQIP (Environmental Quality Incentives Program) or the agency’s TIP (Transition Incentives Program).

#3: The Lack of a Risk Management Tool

Thanks to market maturity, considerable infrastructure, and robust export demand, conventional growers are better able to pursue various marketing strategies or even futures to protect themselves from market price swings. This luxury isn’t available to organic producers and leaves them at the mercy of the market.

Conventional growers can forward contract, and then manage price risk based on precise information around supply, demand, and price. Organic growers may choose to forward contract, but it’s often based on very little objective information. This vulnerability for organic growers highlights the importance of needing the most timely and accurate market data to help them make informed decisions.

Even with these challenges in place, growth in U.S. organic farming will continue. We encourage customers to track domestic acreage growth via our Annual Acreage Report, and to identify local markets through our Facilities Map. With growing infrastructure and more informed growers armed with the right data, organic farmers will eventually be able to realize some of the same advantages conventional growers have today.

To learn more about Mercaris research and market insights, read about our team of experts

Latest Posts

Latest Posts

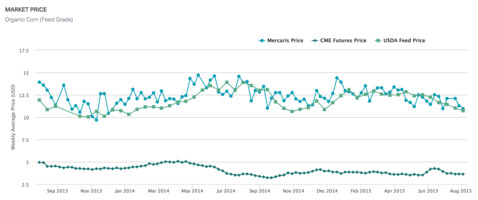

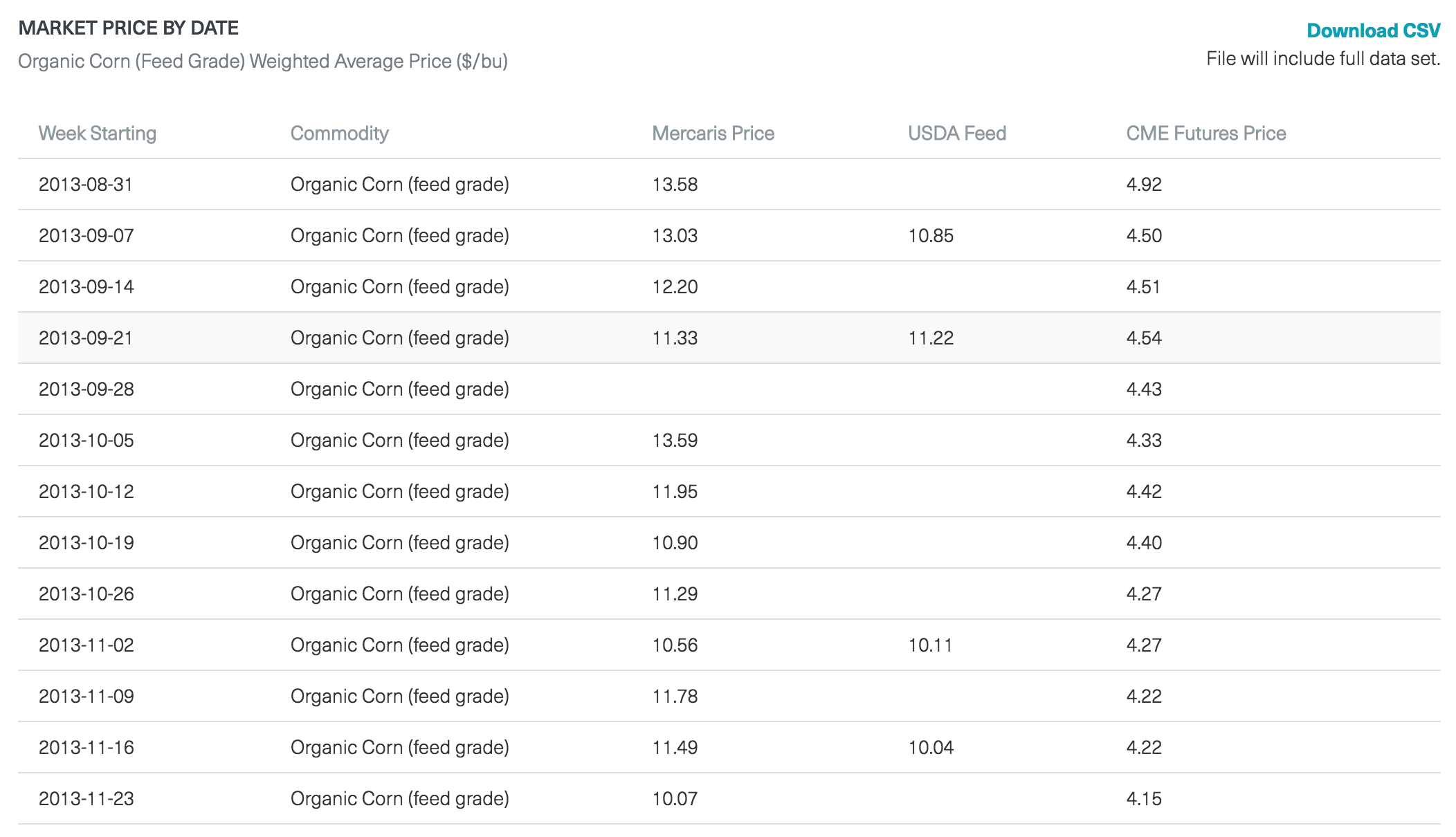

Latest Commodity Prices

Latest Commodity Prices