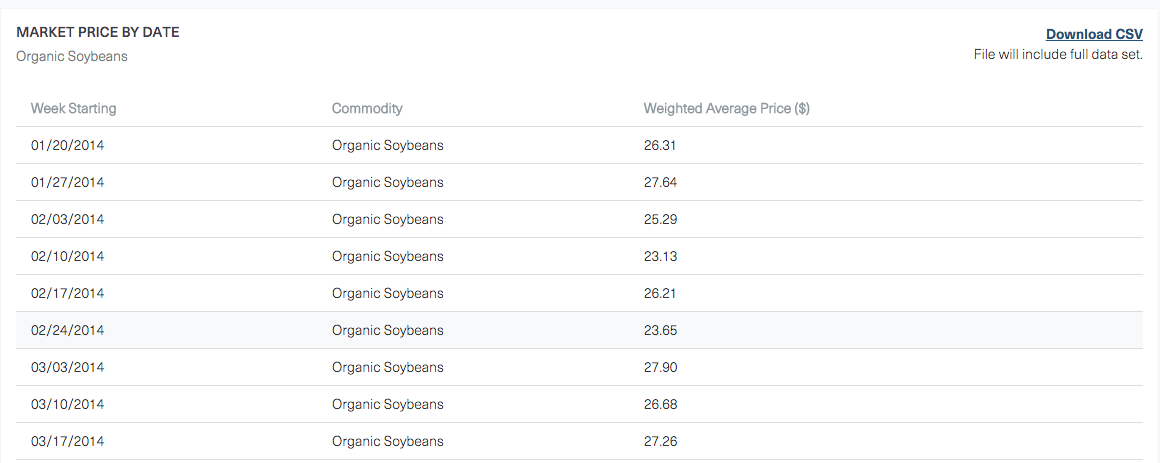

November 8, 2022 (Silver Spring, MD) – The 2022/23 marketing year is expected to be another period of volatile prices for U.S. organic markets. Following two years of increasing prices, the U.S. organic soybean harvest is expected to set records during Fall 2022. The result of this occurrence is expected to be bearish price pressure for organic soybeans into the first half of 2022/23 and a significant reduction in imports over the second half of the marketing year as discussed in the Fall 2022 Mercaris Commodity Outlook.

While organic soybean prices are expected to fluctuate, organic corn looks to remain steady for the foreseeable future.

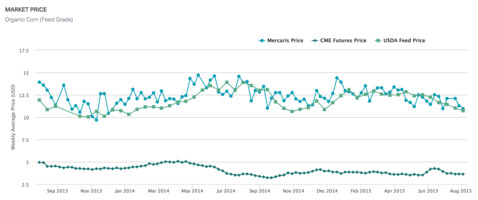

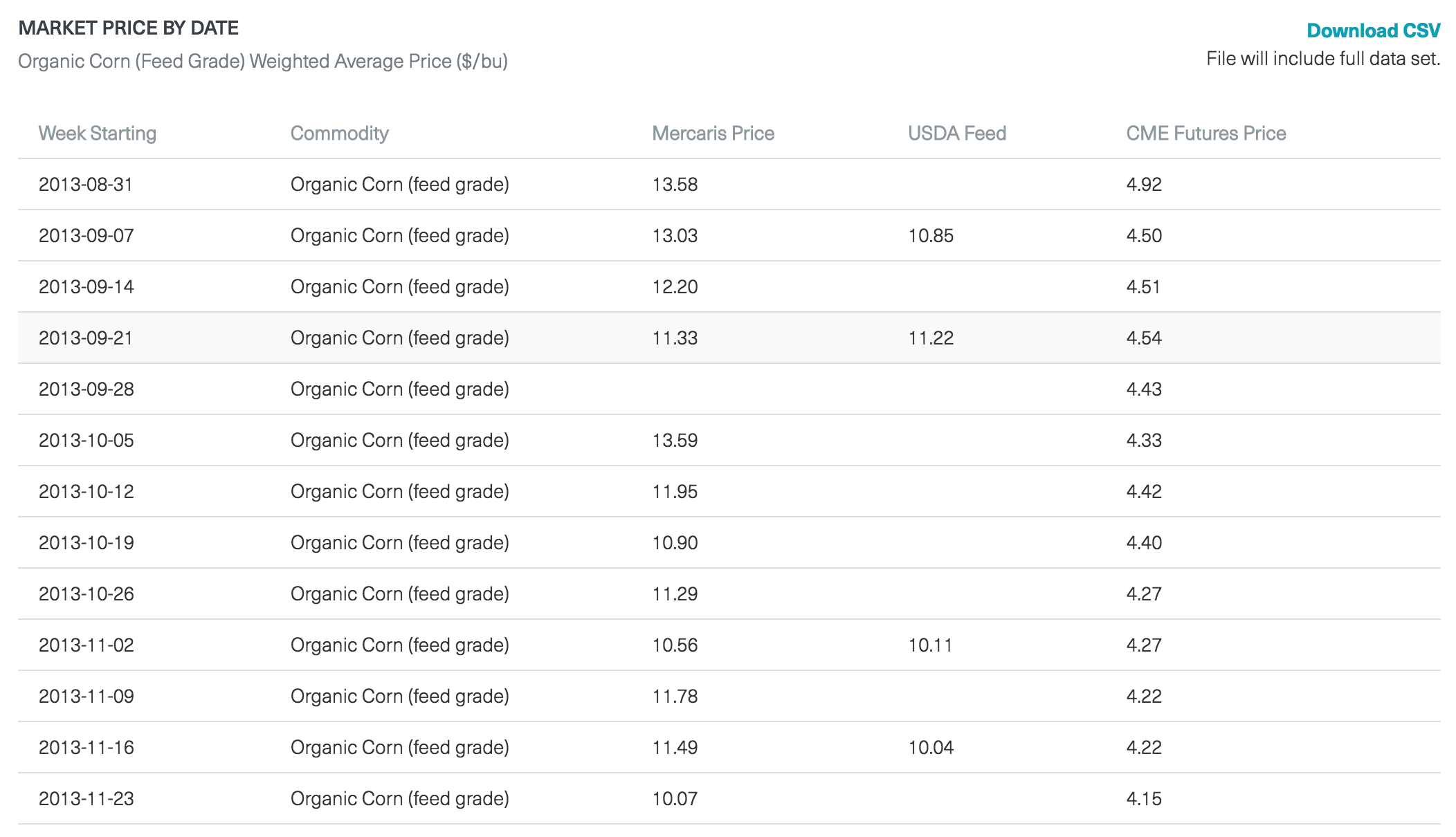

“We estimated 2022/23 began with large carryover stocks of organic corn. However, U.S. organic corn production is expected to decline this fall, largely offsetting these carryover stocks and keeping prices supported through harvest,” says Ryan Koory, Vice President of Economics with Mercaris. “Furthermore, the outlook for U.S. organic corn imports is expected to be bullish for prices as supply issues in Argentina, Canada and the Black Sea region reduce U.S. imports of organic whole and cracked corn. As a result, Mercaris anticipates bullish support for U.S. organic corn prices will persist through the Spring 2023 and into the fall.”

Improving organic spring wheat yields over 2022 are expected to add to total U.S. organic wheat supplies. Despite this improvement, 2022/23 production is expected to remain below 2020/21 levels, keeping supplies generally tight and bullish support under prices. Additionally, growing conditions for much of the U.S. High Plains have remained dry through 2022 leading to mixed wheat quality, elevated protein levels and an uncertain 2023/24 organic winter wheat crop outlook.

“With bullish price expectations for organic corn as well as organic wheat and an outlook of weaker prices for organic soybeans, Mercaris projects Spring 2023 will see an oscillation of U.S. organic acreage away from organic soybeans,” says Koory. “Mercaris projects U.S. organic soybean area could decline by as much as 25 percent over 2023/24. Half of these acres are expected to rotate into organic corn with organic spring wheat area expanding slightly as well.”

With these acreage shifts and import expectations, Mercaris projects prices for organic corn and wheat will move lower over the last half of 2023, while organic soybean prices find support. However, this outlook is heavily dependent upon no additional trade disruptions developing over the coming year and U.S. weather patterns facilitating more typical growing conditions.

The information above is summarized from the Fall 2022 Mercaris Commodity Outlook. To find more details and information on other organic and non-GMO markets, visit www.mercaris.com.

About Mercaris

Mercaris has helped its customers capitalize on the growing demand for organic and non-GMO agriculture by providing market intelligence, analysis and trading services exclusively for the identity-preserved agriculture industry. Mercaris hosts the largest organic and non-GMO grain and oilseed market survey across the U.S. as well as Canada and recently launched an organic dairy initiative. The company also maintains a trading platform for organic and non-GMO commodities. With a dynamic combination of data, insights and technology, our customers can access solutions for every challenge. For more information visit: www.mercaris.com.

Latest Posts

Latest Posts

Latest Commodity Prices

Latest Commodity Prices